Most DeFi yields are quoted without context. Aave pays X percent on USDC. Morpho pays Y percent. USDe earns Z percent. The numbers look attractive, but they don’t tell you what risks you are being compensated for.

This article does something simple. It takes the credit pricing framework that bond markets have used for a century, applies it to supplying stablecoins on Aave and Morpho, and shows what a fair yield should look like. It then runs the same exercise for USDe and shows that the additional risk over USDC is smaller than most people assume. Finally, we look at one of Altitude Fund’s current positions and the risks that come with it.

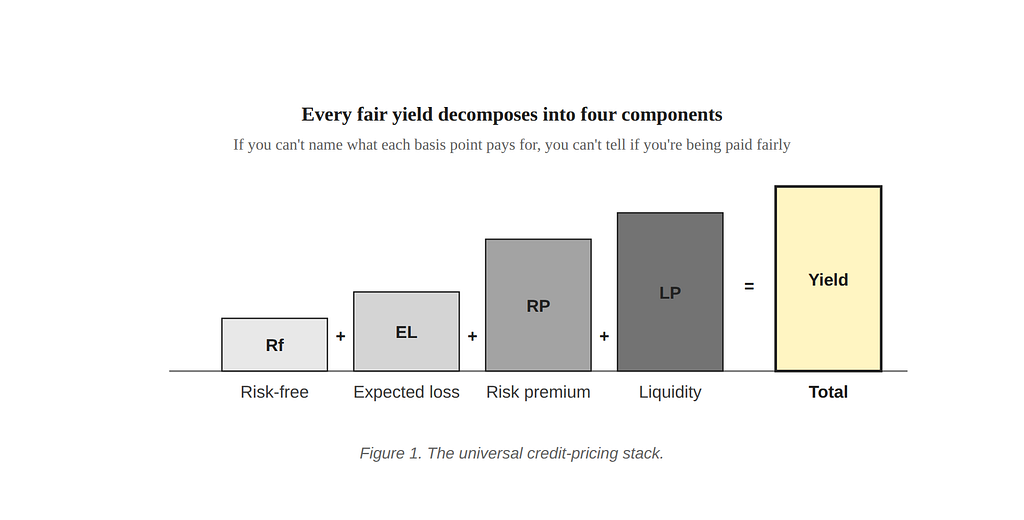

Every yield is a stack of compensations

Whether it’s a Treasury bond, a junk bond, or a DeFi deposit, every yield decomposes into the same four components:

Yield = Risk-Free Rate + Expected Loss (PD × LGD) + Risk Premium + Liquidity Premium

The risk-free rate is the floor, what Treasuries pay for zero credit risk. The expected loss is the actuarial cost of doing business: probability of default times loss given default (PD × LGD). It reimburses you for predicted losses; it does not pay you for taking risk. The risk premium compensates for uncertainty around the expected loss. Two assets can have identical expected loss but trade at different yields because one carries a higher risk premium. The liquidity premium pays you to lock up capital you cannot quickly recover; the longer and harder the exit, the higher it should be.

Why a Treasury sets the floor

The risk-free rate is benchmarked to US Treasuries because Treasuries are the closest real-world instrument to a no-default asset. The US government has never defaulted on dollar-denominated debt, can issue currency to meet its obligations, and the secondary market for Treasuries is the deepest in the world. A 3-month T-bill at 4.10% pays you 4.10% for taking essentially no credit risk and essentially no liquidity risk. Every other yield has to be higher than this by enough to compensate for whatever additional risks the instrument carries. If a corporate bond paid less than the Treasury, no one would buy it.

How private credit reaches 9%

Private credit loans are senior secured loans to middle-market companies, held by private credit funds, and they yield around 9% in current markets. Let’s decompose that for practice. Start with the 4.10% risk-free rate. Add expected loss of roughly 1.5% (3% annual default probability times 50% loss given default, since these loans are senior secured against company assets). Add a risk premium of roughly 1.5% for the variance around that expected loss. Add a liquidity premium of roughly 2%, because these positions cannot be sold on a screen; exits require either fund redemption windows or secondary-market negotiations at a discount. The sum lands at about 9%, which is roughly where the market clears. Note that direct lending borrowers do not default dramatically more often than public high-yield issuers, so the extra yield over high-yield (around 7%) is almost entirely liquidity premium. You are being paid roughly 2% to lock up capital.

The same decomposition applies to any yield. The components and their sizes change, but the structure holds.

This is the discipline. Whenever someone quotes a yield, decompose it. If you cannot identify what each component is paying for, you have no way to evaluate the trade.

Supplying USDC on Aave or Morpho

Let’s start with the most basic DeFi credit position: lending USDC into a lending protocol. You deposit USDC. Borrowers post collateral (typically ETH, wBTC, or other tokens) and borrow your USDC. You earn interest.

On the surface this looks like a money market product. It isn’t. You are accepting a specific set of risks that have no analog in traditional cash management.

The four DeFi-specific risks

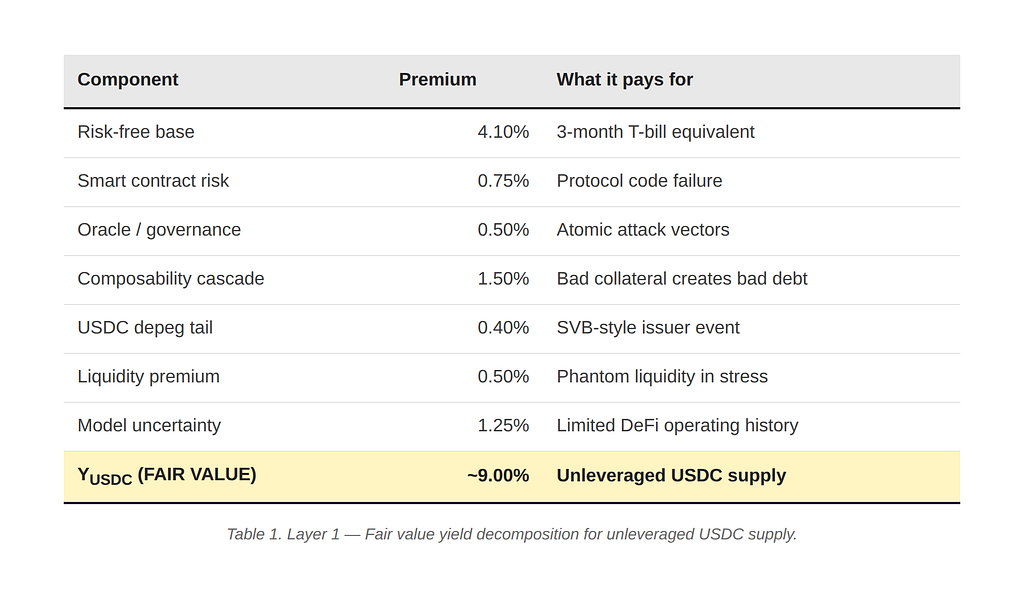

Smart contract exploit risk.The protocol’s code may have a vulnerability. Reentrancy attacks, missing access controls, faulty input validation: bugs like these have drained billions from DeFi protocols. Recovery is rare. The 2022 Ronin and Wormhole exploits (roughly $625M and $325M) were “recovered” only because their sponsoring companies absorbed the loss to protect their brand. That is not credit recovery; that is a shareholder bailout you cannot price into your model.

Oracle and governance risk. Lending protocols depend on price oracles to value collateral and loans. If an attacker manipulates the oracle (typically by flash-loaning a position to distort a DEX price), the protocol makes catastrophically bad lending decisions. The 2022 Mango Markets attack drained $114M this way. Governance attacks, where attackers accumulate tokens to pass malicious proposals, work similarly. The Beanstalk protocol lost $182M in a single block to this mechanism.

Composability cascade. This is the most dangerous because it is the least auditable. Lending protocols accept various tokens as collateral. If any of those collateral tokens fails (a bridge exploit, an LST depeg, a yield-bearing token losing its backing), the lending protocol takes on bad debt even if its own code worked perfectly. In April 2026, attackers exploited a vulnerability in Kelp DAO’s LayerZero bridge to mint roughly 116,500 unbacked rsETH. They deposited it on Aave V3 as collateral and borrowed real WETH against it. Aave’s code worked exactly as designed. Aave’s WETH suppliers were left facing an estimated $120 million to $230 million in bad debt, created in well under an hour.

Stablecoin issuer risk. USDC itself is backed by Circle’s reserves at regulated US banks. In March 2023, USDC briefly traded at $0.87 when Circle’s exposure to Silicon Valley Bank became public. The peg recovered, but a leveraged position would have been liquidated at the low. Even unleveraged depositors face the risk that the stablecoin they hold loses its peg.

All of these risks raise the probability of default, which is what makes this different from TradFi.

Fair value for USDC supply

With those risks laid out, we can build the fair-value stack for supplying USDC. Adding the four DeFi-specific components on top of the T-bill floor, Altitude Fund’s analysts calculate a fair value for unleveraged USDC supply on a top-tier DeFi lending protocol of approximately 9 percent.

Now compare that to what the market actually pays. Aave’s USDC supply rate has averaged 4 to 6 percent in normal conditions. Morpho’s curated USDC vaults generate up to 8 percent, depending on the curator and the underlying market parameters.

Aave at 5 percent is materially underpriced. Even though the market is highly liquid in normal conditions, it is paying you roughly the risk-free rate plus a fraction of the expected loss line. It is not compensating you for composability risk, model uncertainty, or any meaningful risk premium.

Now supply USDe instead

When you supply USDe (or its staked version, sUSDe) on Morpho instead of USDC, you take on every risk we just listed, plus the risks specific to USDe itself.

That raises a question: how much riskier is USDe than USDC as a stablecoin issuer?

USDC is backed by Circle’s reserves at regulated US banks, primarily short-term Treasuries. The peg mechanism is simple: mint and redeem against fiat reserves at $1.00.

USDe is structurally different. Ethena maintains USDe’s peg through a delta-neutral strategy: long spot ETH or BTC, short an equal notional in perpetual futures. The dollar value of the combined position is theoretically constant regardless of ETH’s price, so 1 USDe stays redeemable for $1 of collateral value. The yield on sUSDe comes primarily from funding rate payments on the short perp leg.

This mechanism introduces three risks that USDC does not have:

Exchange counterparty risk. Ethena’s short perp positions sit on centralized exchanges. If an exchange fails operationally (hack, insolvency, regulatory seizure), Ethena loses the collateral on that exchange. Off-exchange settlement custodians (Copper, Ceffu, Fireblocks) mitigate this, but the margin held on the exchange can still be 5 to 15 percent of the position. Lose that, and the hedge breaks.

Forced liquidation of the hedge. When ETH rallies sharply, the short loses money in real time. If ETH gaps up 15 to 20 percent in minutes, the exchange’s auto-liquidation engine does not wait for treasury operations. The short gets force-closed at the worst price, and Ethena is left holding only the spot side. At that point it is no longer delta-neutral, and if ETH then drops, the collateral drops with it.

Funding rate inversion. The yield on sUSDe is not a passive coupon. It is the realized funding rate Ethena captures. ETH perp funding has been negative on roughly 15 to 25 percent of trading days historically. Sustained negative funding depletes the reserve fund and stresses the peg mechanism.

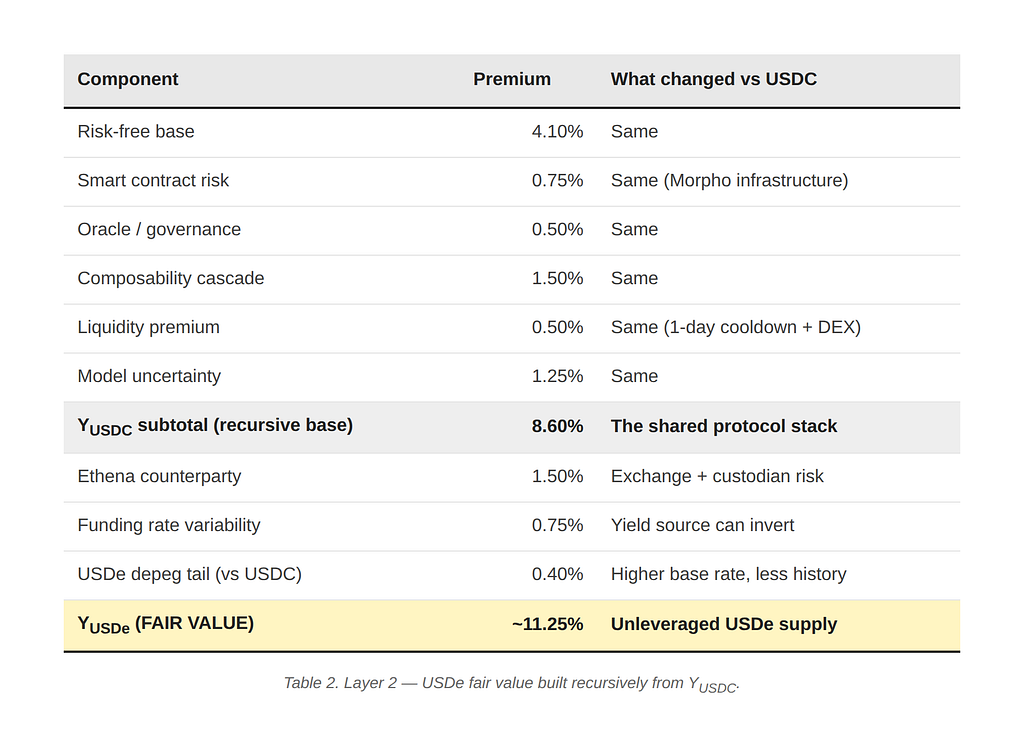

Therefore we can use the same formula, but this time take USDC fair value yield we calculated above as our new risk free rate:

Add all the token specific risks to the USDC’s fair value yield to the yield for USDe:

How do we measure the risk of the leverage?

USDe is not a stablecoin backed 1:1 by USD, and it is not GENIUS Act compliant. The FDIC will not be able to step in the way it effectively did for USDC when Silicon Valley Bank collapsed. If any of the risks above materialize, the chance of a complete depeg is much higher than the chance of USDe slipping to $0.94 or lower and then recovering to $1. So, to mitigate that risk and to keep the fair-value calculation clean, we use a Nexus Mutual insurance policy to cover all of the USDe equity in the looping position.

To calculate the fair-value yield of USDe, you take USDC as the risk-free rate and add the additional risks that raise the probability of default, along with the risk premium. That brings the fair value for unleveraged USDe supply to roughly 11.25%.

Our position: looped sUSDe / USDe at 7x

We hold a leveraged version of this trade: supplying sUSDe as collateral, borrowing USDe, and looping to 7x leverage. The position generates a net 16 to 18 percent on equity.

It may seem obvious that a leveraged stablecoin loop has a fundamentally different risk profile than unleveraged supply, because any brief depeg liquidates the position before it can recover. We see it differently.

Our view is that USDe is more likely to fail catastrophically than to wobble and recover. The mechanism that backs USDe, a delta-neutral position spread across centralized exchanges, does not have a soft-failure mode the way USDC’s banking exposure did during the March 2023 SVB event. If Ethena’s hedge breaks (exchange counterparty failure, custodian failure, or sustained funding stress that exhausts reserves), the depeg is unlikely to be a brief 3 to 4 percent touch that recovers. It is more likely to be a structural, persistent loss of backing.

This matters because the canonical bear case for leveraged USDe loops, “you get liquidated on a recoverable wobble,” assumes the wobble scenario is the dominant tail. We think the dominant tail is the structural-failure scenario, in which leveraged and unleveraged holders lose comparably. Brief recoverable depegs are possible, but given the mechanism they are less probable than the full-failure case.

On top of that, we carry Nexus Mutual cover against a USDe depeg. Nexus covers all of our equity if USDe depegs by at least 6%. Given our health factor of 1.07, our liquidation threshold sits below that level. This removes the single risk that distinguishes our leveraged position from unleveraged USDe supply.

With insurance covering the depeg tail, the residual risks on our leveraged position are the same risks an unleveraged USDe supplier carries: Morpho protocol risk, composability cascade, smart contract risk, and Ethena counterparty risk.

Those risks are not zero. But they are the risks we have already concluded are approximately fairly compensated by Morpho’s roughly 11.25% fair-value yield on unleveraged USDe supply.

If the unleveraged risks deserve about 11.25%, and our leveraged position carries approximately the same risk profile after insurance, then we should take the leveraged trade if it pays more than 11.25%.

Indeed it does. At 16 to 18 percent net on equity, the position pays 500 to 700 basis points above the fair-value yield for what we judge to be a similar risk profile.

Nexus Mutual coverage has policy terms, a claims process, and counterparty risk on the mutual itself, so it is not a perfect hedge. Our judgment about the shape of Ethena’s failure distribution could be wrong. And leverage always carries operational risk around health-factor management, gas costs during liquidation cascades, and oracle pricing under stress. We size accordingly.

None of this makes DeFi safe. The composability cascade risk behind the Aave and Kelp DAO event in April 2026 is real, and it is priced into the framework. But once you accept that you take that risk by supplying any stablecoin to any DeFi lending protocol, the marginal decision between USDC and USDe is much smaller than it first appears.

Fair Value Yield: What Are You Actually Being Paid For in DeFi? was originally published in Altitudedp on Medium, where people are continuing the conversation by highlighting and responding to this story.