USDe was built on funding rate yield. Most of that engine is now gone, replaced by lending.

For two years the answer to “where does sUSDe yield come from” was simple. Ethena held spot crypto, shorted an equal amount of perpetual futures, and collected the funding that long traders paid to hold their positions. The position carried no price exposure and the funding paid the holders. When the market ran hot, the yield ran high.

That is no longer the main story. Over the course of 2026 Ethena rebuilt the backing of USDe, and the basis trade that defined the protocol is now a minor part of the reserve.

Two forces pushed the shift. Funding compressed and concentration became a liability.

Funding rates cooled from the 2024 highs, so the trade that once paid double digits now pays single digits. At the same time Ethena had built a very large protocol on a single source of yield that depends entirely on speculators staying net long. A reserve committee was formed and the protocol began moving capital into assets that pay in a steadier way.

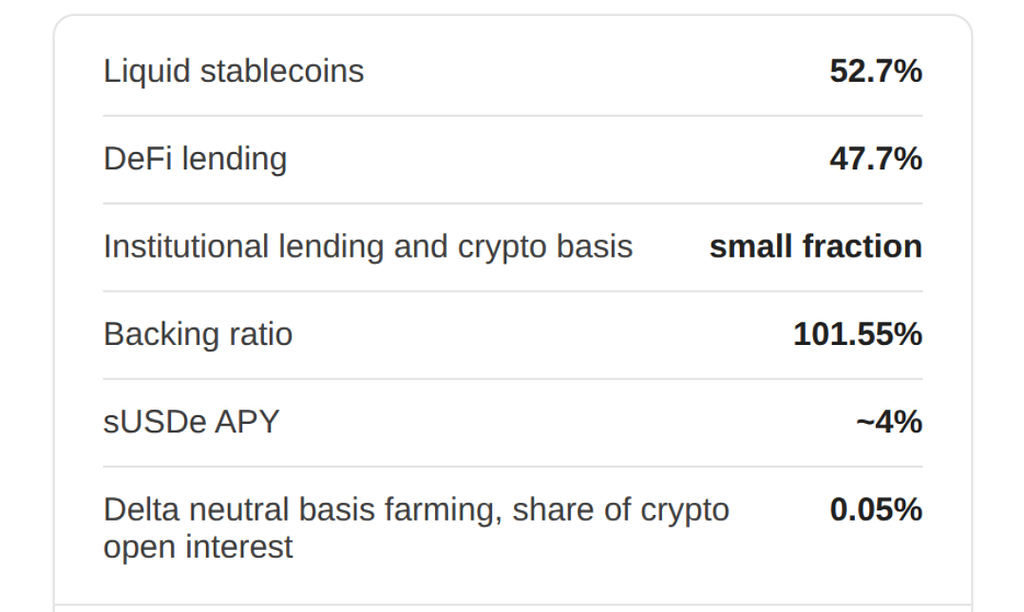

The transparency dashboard tells the story directly. As of late May 2026 the backing looked like this:

A protocol once known for running one of the largest short books in crypto now holds a tiny slice of open interest. The derivatives position did not vanish, but it stopped being the point.

The largest active component is DeFi lending earning borrow rate. Alongside it, Ethena has been signing overcollateralized lending agreements with institutional desks, including Anchorage Digital, Maple Institutional, and Coinbase Asset Management, and has floated the idea of acting as a prime broker that lends against client exchange balances. The reserve framework also opens the door to real world credit and to basis trades outside crypto, in equities and commodities, run under set risk limits.

The old failure mode was funding inversion and exchange counterparty stress, the kind of event where the short leg starts paying instead of receiving. That risk is minimal if not negligible. In its place sits credit and liquidity risk. The yield now depends on borrowers repaying, on lending venues staying solvent, and on stablecoin reserves staying liquid when holders want out. For anyone holding sUSDe, or looping it, the question to ask is no longer “what is funding doing.” It is “who is Ethena lending to, and what happens to that book under stress.”

The peg held near a dollar through the change and the backing stayed above full. The product is calmer than it was. It is also a different product than the one most people bought.

We read this as two changes at once, and we do not love both of them equally.

The part we are skeptical of is focus. Ethena’s real edge was running the basis trade at a size almost no one else could match in DeFi. The custody setup, the exchange relationships, the execution across venues, that is a moat, and it is theirs. DeFi lending and institutional credit are crowded rooms. Maple, the Morpho curators, and TradFi desks already do this work, and the yield Ethena earns there is mostly the market borrow rate that anyone can earn. When you move from a thing only you can do well to a thing everyone does, you trade a moat for a commodity. A protocol that tries to be a basis fund, a credit desk, and a stablecoin issuer at the same time risks being average at all three.

And the kind of trust I am giving changes with it. As an asset manager holding USDe or sUSDe, I am no longer trusting Ethena the specialist who runs one well defined trade. I am trusting Ethena the asset manager, and every allocation it makes. Now every lending venue they choose, every counterparty they underwrite, and every allocation the risk committee signs off on becomes our exposure. I am backing a discretionary book and the judgment behind it, which is a far wider surface to diligence and a far harder thing to verify from the outside.

The part I like is the return structure. Funding yield is sharp and unreliable. It spikes, it fades, and in the wrong market it turns negative and the protocol pays to hold the hedge. Lending yield is duller and far more dependable. It cannot go negative, it does not depend on speculators staying long, and it gives holders a return they can actually plan around. For a token that wants to be used as money and as collateral, boring is the right ambition. The lower odds of a zero or negative yield month make sUSDe a steadier base to build on, which matters a lot if you are levering it.

Ethena gave up some of what made it special in exchange for a return that is calmer and harder to break. If the goal is to be a high yield trade, this is a step down. If the goal is to be a real stablecoin, this is the step it had to take. I think they chose the second goal on purpose, and on that goal it is the right call.

Ethena stops farming the basis was originally published in Altitudedp on Medium, where people are continuing the conversation by highlighting and responding to this story.